stETH Depegging: A Case Study of Cascading Events

Published:

Aug 18, 2022

Authors:

William Starr

Liang Wu

Share:

Financial markets are a complex set of interlinked systems. Decentralized finance (DeFI) markets are even more complex: they move faster, are global in nature, and are infinitely more composable. These characteristics, unique to DeFi markets, have always been a feature, not a bug. And they’re especially critical to those who have been underserved by traditional finance. The goal of DeFi is to build financial rails that are open, transparent, and accessible to anyone in the world.

However, complex interlinked systems like decentralized finance are at greater risk of suffering from cascading events. Cascading events are events that take place through a chain reaction and are often uncontrollable and happen in quick succession. Cascading events can occur in a part of an ecosystem and quickly snowball to impact the broader ecosystem. An apt metaphor is when one domino falls, the next one follows, so on and so forth.

Web 3 users, builders, investors, community members, contributors and etc, can learn alot from cascading events: everything from protocol design to market psychology to how complexity builds upon different aspects of the market.

Today, we look at Lido’s stETH token, specifically the stETH depegging from its social and market consensus peg to ETH that happened in June 2022 as a case study to understand cascading events. Particularly, looking at how cascading events can occur in a part of the ecosystem and quickly snowball to create far-reaching impact on the broader ecosystem. From this case study we also share some observations and learnings.

Let’s jump right in!

What is Lido?

Lido is a DeFi protocol that allows anyone to stake their ETH to secure the Ethereum Network. In exchange, the staker is paid a management (service) fee taken as a percentage of the rewards. This fee is a small percentage of the rewards allocated to your portion of staked ETH.

Lido is a very important part of the Ethereum ecosystem. The company was created to make staking on Ethereum more accessible to the average token holder and validator. In a Proof of Stake system (which Ethereum is soon moving to), token holders who stake their tokens earn rewards for securing the network. See [here] for a primer on what the move to Proof of Stake means for Ethereum.

Without Lido, the requirements to participate in Ethereum’s Proof of Stake are significant :

A token holder needs to stake 32 ETH to create a validator node. At current prices (August 2022), 32 ETH is about ~$50K+ USD. At all time highs (ATH), that’s closer to $150K USD. Not an insignificant amount for the average token holder.

There are technical requirements to spin up a node (e.g. deploying code)

Previous operational knowledge is necessary to run and optimize a node

If a validator messes up or makes a mistake, their entire stake can be removed by the network – also known as slashing.

So… the criteria for participation is strenuous, and the stakes are high. All this can be a tough pill to swallow for the average token holder looking to be a validator.

In short, Lido lowers the barriers to entry to become a network validator, allowing more token holders to participate in securing the Ethereum blockchain. Lido allows users to become network validators by staking any amount of ETH in their protocol (rather than the typical 32 ETH required), no technical know-how needed.

The Lido protocol is decentralized. Rather than using a centralized approach, Lido uses a consortium of verified and trusted validators to “manage” the actual staking and node operation on behalf of the users. Users can also influence the project's direction through the $LDO token, which enables users to participate in governance over the protocol itself.

stETH: Liquidity on Top of an Illiquid Asset

Currently, ETH is staked only on the beacon chain and cannot be withdrawn. Withdrawals of ETH staked will NOT be available until months after the merge has occurred (during the Shanghai hard fork).

To allow users to exit their position now, Lido created $stETH – a liquid tokenized version of the staked ETH users deposit. When a user locks up (or ‘stakes’) 1 ETH in Lido, they receive 1 stETH in return. In this way, stETH acts like a redeemable receipt. stETH represents the same value as whatever amount of ETH it was deposited for, and functions similarly.

stETH is yield generating because of the underlying staked ETH it represents. But stETH has another utility feature, too: it can be traded.

Have your cake and eat it too.

In a perfect world, then, 1 stETH should be worth at least 1 ETH, if not more when accounting for the underlying staking yield attached. (Of course we don’t live in a perfect world, and 1stETH usually trades at a slight discount to 1 ETH, mainly due to (1) stETH is not redeemable for the underlying ETH and (2) stETH is newer and haven’t been as tried and tested compared to ETH).

All this enables further liquidity in the broader DeFi market. Liquidity is critical to healthy DeFi markets. Liquidity literally enables markets to exist. And when you have a token like stETH, whose key feature is liquidity on top of an illiquid asset, a market forms and with it, arbitrage opportunities arise.

Lido has seen strong demand for the products and services described above, commanding a significant amount of market share. In fact, stETH token accounts for ~90% of liquid staked ETH and almost ⅓ of all ETH staking goes through Lido’s network.

This all sounds great: A fledgling ecosystem created to secure the Ethereum network in a trustless and decentralized manner by increasing user participation in ETH staking.

Where could it go wrong?

Chasing Yield with stETH

Nothing in crypto exists in a vacuum. It’s important to contextualize stETH in the broader financial market itself.

Over the last few quarters, CeDeFi (Centralized DeFi) institutions and crypto funds started taking on leveraged bets with stETH and ETH to maximize yield. CeDeFi products allow customers to gain exposure to crypto while managing custody and interaction with the underlying tech themselves, in-house. The institution is centralized, but they provide products to customers that inherently depend on DeFi.

Like many trading strategies, CeDeFi institutions combined a variety of DeFi Lego blocks (See this post to learn more about Money Legos).

These leveraged bets were typically conducted on Aave/Instadapp, and worked like this:

Stake ETH in Lido, receive stETH in return.

Deposit stETH into Aave and borrow ETH.

Rinse and Repeat.

By levering up their exposure to stETH, CeDeFi institutions were able to greatly compound the interest they would earn as compared with just simply staking their ETH. This, however, came at the cost of resilience. Levering exposure to stETH made CeDeFi institutions significantly more sensitive to any potential issues that could arise, no matter how unlikely they seemed at the time.

All of that leveraged CeDeFi institutions created during this time was predicated on the assumption that 1 stETH is relatively equal to 1 ETH, even if it was technically not yet redeemable.

If the “1 stETH is relatively equal to 1 ETH” assumption is true, which it would be under normal market conditions, the leveraged plays would be just fine… right?

Assumption Breaks: stETH depegs from ETH

By May 2022, the crypto markets were already very shaky. Macro conditions had taken a turn for the worst, and on-chain yield opportunities were drying up as people started trading less. On top of that, the Terra blockchain crash had an immediate and dramatic effect on the entire DeFi ecosystem. See here for a detailed timeline of Terra. By mid-June 2022, the Terra blowup contagion reached stETH. Even though Terra is a completely different chain, the composability across different chains created a delicate interlinked system that came back to bite us when things blew up.

One of the products offered on Anchor (Terra’s lending protocol) was taking wrapped stETH and using that as collateral on their chain. This collateral essentially became trapped because 1) nobody could repay those loans to get their collateral (wrapped stETH) back on Terra, and 2) the Terra network shut down completely so it was impossible to access those tokens anyways.

The people and entities using the Terra network were also the same ones using these leveraged yield products for stETH. Not only did they lose access to those funds, but a majority of their capital (including a “stable” asset) evaporated from the Terra fallout. This put those funds in a precarious condition that could lead to a “bank run.”

The only way to unwind this was to sell stETH to cover their positions – creating selling pressure on stETH.

This started the stETH price depegging causing liquidations in the positions held on Aave.

The fundamental assumption for the stETH:ETH peg was being challenged.

With 1stETH no longer closely equaling 1 ETH, cascading liquidations quickly ensued. As little as a 10% variance was enough to cause the collateral ratio to fall below the liquidation cutoff, due to how leveraged the loans were that these institutions had created. The cascading effects start with the riskiest and most leveraged ETH borrowers (who have the highest loan-to-value ratio) getting liquidated and having their stETH automatically sold on the open market. This selloff caused low liquidity in the stETH:ETH Curve Pool, which then created further sell pressure. This then led to more cascading liquidations, so on and so forth.

The market couldn’t unwind this trade.

Under normal circumstances, lenders were happy to lend out ETH as long as stETH was provided as collateral: the large demand and established consensus on price parity made for a comfortable situation. But, as the lending became more risky, all that liquidity dried up because no one wanted to lend out ETH – a truly liquid asset – for stETH, an asset representing an illiquid version of non-redeemable ETH.

Who would want to lend ETH in this scenario? Would you choose to at all?

Under stable conditions, when a price depegs on a DeFi Protocol like Curve, market makers step in and arbitrage by market selling ETH for stETH. In this situation, there was greater demand for ETH than stETH. While there’s still no true way to redeem ETH with stETH, there was established market consensus that the two assets closely followed each other in price. Under small swings, market markers can arbitrage and make a quick profit. However, in this case, stETH began dropping even further relative to ETH. Mercenary capital quickly cut their losses and sold their positions, or removed their liquidity from the pool entirely.

Market makers have to protect their own books – it's existential. If you don’t cover your book (a.k.a. your own leverage positions) then you go under. To cover their losses, the market makers involved in the blowup had to sell stETH at a price less than 1 ETH.

The sell pressure this put on stETH caused the price to crash further, leading to a series of cascading events:

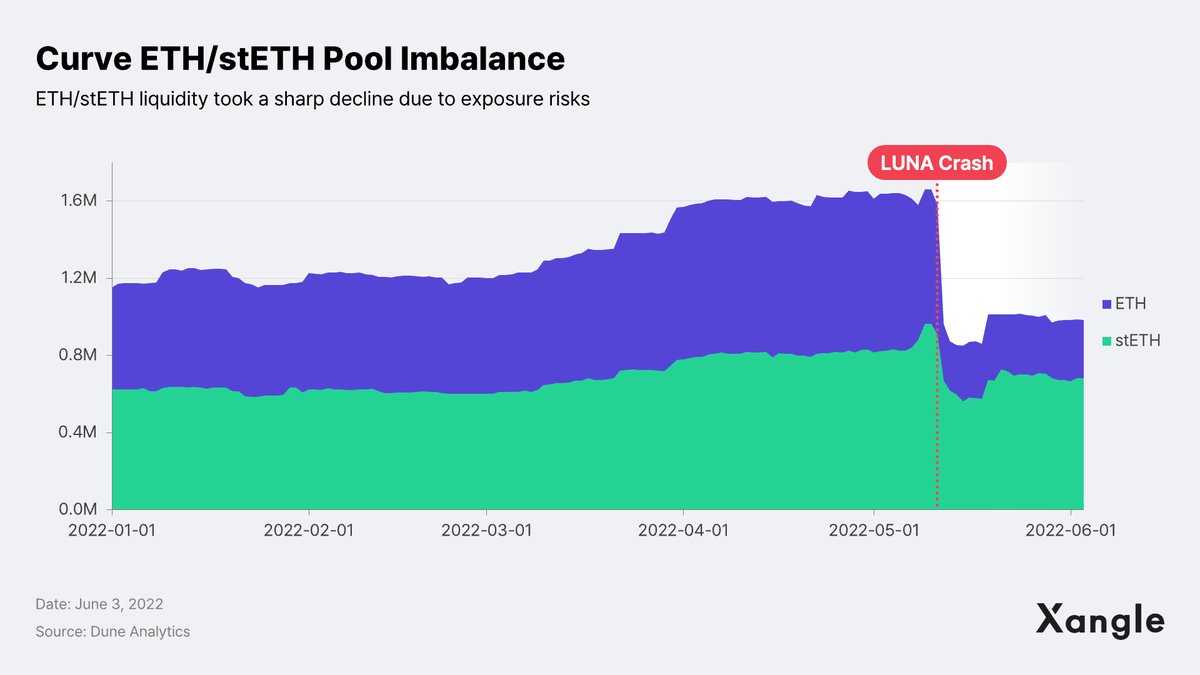

First, reserves in the Curve protocol crashed. Everyone wanted to trade their stETH for ETH, and in a short amount of time, the quantity in the stETH pool was greater than ETH in the Curve pool. At one point, only 20% of the liquidity pool was ETH, compared to a normal 50%. Everything was out of balance… 1 stETH was no longer 1 ETH, and anyone trying to sell stETH would face extreme slippage.

Second, this then led to a near liquidation of Celsius’ (a CeDeFi institution with one of the largest positions of stETH) position in Aave almost being liquidated. Once those first bad debt positions started to get hit and unwind, the on-chain price oracle dropped precipitously.

Narrowly avoiding complete liquidation and catastrophe of the position, Celsius has fully paid back the loan on Aave, and no longer has an active stETH collateral position. This has allowed the peg to return to a healthy variance (~2%). The markets have now recovered relatively well from the turmoil of these past few months.

Cascading Events and Downward Spirals

Similar to historical corrections in the crypto market, few could predict the significance (and rapid succession) of these events.

It almost always feels unprecedented.

What learnings and observations can we come away with?

Market and consumer psychology can break fundamental assumptions.

Market and consumer psychology is very volatile. Even only a slight depegging of stETH:ETH could cause FUD (Fear, Uncertainty and Doubt) and rattle a fragile market further. Everything about 1stETH equaling (at least) 1ETH makes sense, yet in fragile market conditions, people were willing to sell 1stETH for less than 1ETH to cover their losses. The market psychology at the time was not strong enough to handle the stETH:ETH-depegging and defaulted to the natural instincts of self-preservation.

Dual Nature: The key feature can also be the key bug.

The critical feature of stETH became the critical bug in stETH. Liquidity is good, but liquidity to over-leverage on one thing can be bad. It’s good to have money legos, but sometimes the strongest feature may end up being the weakest link. It depends on market conditions. Complex, interlinked systems create greater opportunities for the acceleration of widespread contagion.

In Web 3, it is important to create open forums to gather community feedback, pressure test product design and continuous testing. And even then, you may not know how things will work in the wild until you inevitably ship the product. The design phase should also focus on designing stop gaps and guardrails.

Game theory got the best of everyone. Everyone wanted to protect their book, not the system.

Not my system, definitely my book.

Many of the token economics during the past few years have focused exclusively on ways to increase Total Value Locked (TVL): the amount of money a DeFi protocol is managing at any given time. This gamification of narratives and hype cycles creates a toxic environment penalizing the last one “holding the bag.” While there is value in protocols optimizing to drive interest and usage through their tokenomics, this needs to be done sustainably and with user protection in mind, otherwise it’ll always be self-preservation over optimization for a healthy functioning system.

Moving forward, a significant topic of discussion will center around strategies that allow protocols to take advantage of reflexive bull market cycles – and how they can protect themselves during that same reflexivity when things aren’t going well. Of related importance is the urgency for protocols to design with inherent protection in mind, ideally baking guardrails into the protocol.

Contagion always surprises us

The hardest part about contagion in any market-based system is that often, it’s difficult to digest the complex implications that arise from an impacted interlinked system. This, coupled with the fact that market behavior sometimes is unexpected and hard to predict.

Murphy’s law is real.

While it sometimes may seem like nothing can go wrong, there is always a chance it does. This chance increases with increasing complexity in protocol design. A system-wide cascade can be caused by a variety of factors that originated in various parts of the system unidentifiable to you. And even after successfully identifying the origin of the problem, you must then embark on a tedious and exertive journey: convincing others you’re right. Seeing contagion in the purview of cultural milieu requires building conviction across multiple parties and entities, all while accounting for their different drivers and incentives.

A healthy market is about balance. When there is an imbalance, expect a correction. When there are significant imbalances, expect significant corrections. In this way, financial markets are similar to systems in nature.

Nature always finds a way to self-correct. It seeks balance.

Balance is the way.

Moving Forward

Lido is an important part of the Ethereum ecosystem. It’s a piece of critical infrastructure that allows for greater participation in decentralized systems like Ethereum.

In our next installment, we’ll take a look at Lido’s governance model. Specifically, we’ll explore:

Community proposals – What is the community proposing?

Pre vs. Post-Merge – How will Lido’s governance differ Pre-Merge versus Post-Merge?

Conditions to thrive – What are the ideal states of a player like Lido, which provide a key piece of infrastructure in liquid staking and the broader Ethereum ecosystem?

Need for adaptation – What do you do as a project when the underlying ecosystem you are supporting is always changing and constantly in-flux?

Scaling & velocity – How do you balance achieving scale versus running the risk of becoming “too big too fail”?

Thanks so much for reading. See you next time!

Author: William Starr

William is an investor and technical lead at Fintech Collective. He's been a builder, adviser and investor in Web 3 and DeFi since 2017.

Social links: Medium; Twitter; LinkedIn

Author: Liang Wu (LJW)

Liang is a Web 3 Research Fellow at HBS and a builder/operator in Web 3 since 2018. He leads Life in Color, a writing collective that explores and breaks down different topics in Web 3.

Social links: Life in Color Blog; Liang Wu

Special thanks to Parker Jay-Pachirat on the Fintech Collective Team for reviewing and providing feedback and edits on this essay.

Disclaimer: This article was written to explore underlying issues and insights in the Lido ecosystem and written for purely educational purposes. Nothing written in this article should be taken as financial advice or advice of any kind.